AANDELE PRYSE IN SA EN VSA EN DIE OORLOG IN DIE MIDDE-OOSTE

Agtergrond

Geopolitieke spanninge het daartoe gelei dat oorlog tussen Amerika/Israel en Iran op 28 Februarie 2026 uitgebreek het. Een van die gevolge van die huidige oorlog is die verminderde olieproduksie en die gevolglike styging in brandstofpryse. Die duurder brandstof raak nie net Suid-Afrikaners se sak wanneer hulle hul motors se tenks vul nie, maar beïnvloed ook die winsgewendheid van Suid-Afrikaanse maatskappye wat op die Johannesburgse Aandelebeurs (JSE) genoteer is.

Suid-Afrika

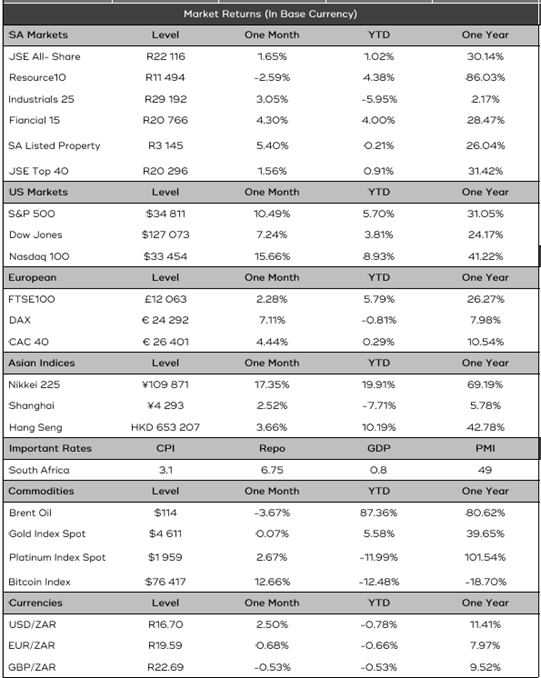

Suid-Afrika vorm deel van die ontwikkelende ekonomieë wat aanvanklik goed gevaar het gedurende die eerste twee maande van 2026, totdat die oorlog op 28 Februarie uitgebreek het. Gedurende Maart 2026 het die JSE All Share Index met 13% gedaal — die grootste maandelikse daling in 18 jaar. Gedurende April het die indeks egter gestabiliseer, maar dit bly sensitief vir energieprysskokke.

Weens die hoër brandstofpryse het Suid-Afrikaanse industriële aandele, kleinhandelaars en eiendomsmaatskappye se aandeelpryse gedaal. Hierdie ondernemings is nou gekoppel aan die plaaslike ekonomie en verbruikersbesteding, wat tans onder druk verkeer. Groot maatskappye met internasionale blootstelling se pryse het ook verswak. Richemont is geraak deur swakker wêreldwye vraag na luukse goedere, terwyl Naspers en Prosus afgetrek is deur swakker prestasie in Chinese tegnologie-aandele.

Die Suid-Afrikaanse geldeenheid het ook ’n belangrike rol gespeel. Die rand het versterk tot ongeveer R16 teenoor die Amerikaanse dollar voordat dit effens verswak het. Hoewel dit positief mag klink, verminder ’n sterker rand die waarde van buitelandse verdienste wanneer dit terug na rand omgeskakel word. Aangesien baie van die grootste maatskappye op die JSE hul inkomste oorsee verdien, het dit hul aandeelpryse verder gedemp.

Amerika

Amerika vorm deel van die ontwikkelde ekonomieë, en hul aandelebeurse is anders deur die oorlog geraak. Suid-Afrikaanse aandele het nie tred gehou met die sterk herstel van die Amerikaanse markte ná die aanvanklike daling in aandeelpryse aan die begin van die oorlog nie. Dit was die gevolg van ’n kombinasie van wêreldwye onsekerheid, die tipe maatskappye wat op elke mark genoteer is, en bewegings in wisselkoerse.

Amerikaanse maatskappye, veral in die tegnologiesektor, het voortgegaan om winsgroei te toon, wat beleggers gelok het. In onseker tye neig internasionale beleggers ook om geld na die VSA te verskuif omdat dit as ’n veiliger beleggingsbestemming beskou word. Suid-Afrika, aan die ander kant, het ’n mark wat meer afhanklik is van kommoditeite en wêreldwye ekonomiese siklusse, wat dit meer vatbaar maak vir skokke.

Samevatting

Daar is ’n gesegde: “Dit is makliker om ’n oorlog te begin as om dit te stop.” Mag diplomate die oorhand kry oor generaals sodat vrede kan terugkeer. Vrede sal olieproduksie verhoog en gevolglik brandstof goedkoper maak. Dit gaan egter tyd neem voordat die huidige hoë brandstofpryse en inflasiedruk verdwyn.

In ’n ná-oorlogse situasie kan verwag word dat die JSE weer sterk sal vertoon, mits inflasie onder beheer bly en rentekoerse nie dramaties verhoog word nie.

NOTA

Ek het in 1983 my meestersgraadverhandeling in Staatsleer aan die Universiteit van die Vrystaat voltooi met die titel: “Islamitiese Determinante in die Wêreldpolitiek.”

Dit is kenmerkend dat die rol van olie in die internasionale politiek gedurende 1970’s, weer 50 jaar later herhaal word. Die prys van ’n vat olie het destyds van 1,80 dollar in 1970 na 3 dollar in 1973 en na 31 dollar in 1979 gestyg. Daar was bewindsverandering in Iran toe die Islamietiese Revolusie in 1979 plaasgevind het. Iran, wat deel van OPEC is, het destyds ook olie aangewend om sy Islamitiese doktrine internasionaal te bevorder.

In die huidige oorlog word olie steeds deur Iran as ’n geopolitieke wapen gebruik om Amerika en ander olie-verbruikende lande onder druk te plaas.

Marksyfers tot einde April 2026