Stop Paying Yourself Last

For many professionals, personal savings are what’s left over — if anything is left at all.

The data is clear: South Africa’s domestic savings rate remains worryingly low. Even among high-income earners, inconsistent or delayed investing is common. Income alone does not create wealth. Behaviour does. The real risk isn’t lifestyle inflation — it’s time.

Missed early contributions cannot be fully recovered later, no matter how high your income becomes. Compounding rewards consistency, not intention. Paying yourself first isn’t about sacrifice; it’s about ensuring today’s success translates into future independence.

If Your Business Needs a Budget, So Do You

No business operates successfully without a budget. Yet many professionals try to run their personal finances without one. Paying everyone else first — the bank, SARS, suppliers, schools, lifestyle — is what happens when there is no clear structure.

Fortunately, a simple framework solves this: the 50/30/20 principle.

- 50% – Essential Expenses

Bond or rent, food, medical aid, school fees, fuel, insurance and other “must-have” costs.

- 30% – Investments (Your Future Self)

Long-term wealth building. Retirement funding. Investments that compound over decades.

This allocation happens before discretionary spending. This is how you pay yourself first.

- 20% – Lifestyle & Discretionary Spending

Travel, entertainment, upgrades, dining out and lifestyle enhancements.

This framework also brings clarity to big financial decisions. If a new home or vehicle pushes your essential expenses above 50%, it is not affordable — regardless of what the bank approves. Affordability is not what you qualify for. Affordability is what fits sustainably inside your structure.

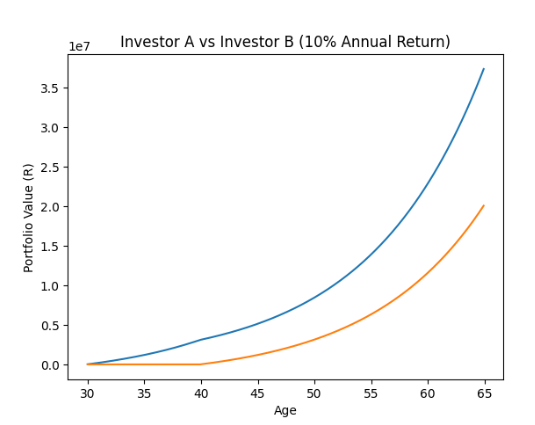

The Cost of Waiting: A Simple Illustration

Let’s consider two investors with similar careers and earning potential.

- Investor A starts investing R15,000 per month at age 30 and contributes for 10 years — stopping at age 40 — but leaves the money invested.

- Investor B delays saving while focusing on practice expenses and family commitments. At age 40, they begin investing R15,000 per month and continue until age 65 — 25 years of contributions.

Assuming the same long-term return, Investor A can still retire with more capital than Investor B despite investing for less than half the time.

Why? Because Investor A gave their money an extra decade to compound. Those early contributions don’t just grow — they grow on top of growth, year after year. By the time Doctor B begins, Doctor A’s capital has already built momentum. Compounding is exponential, not linear. The first ten years are often the most powerful.

Time is the most valuable asset in wealth creation. And unlike income, it cannot be increased later. High income creates opportunity, but discipline creates freedom. If your budget reflects your priorities, your future becomes predictable.

Ruvan J Grobler RFP™ (PGDip Financial Planning)